It is an insurance to safeguard your business in the event of a key person’s death, disability or significant medical event. The term 'key person' refers to an individual whose contribution to the success of the business is significant.

The loss of a key person can have a devastating effect on the financial stability of the business. Key Person Insurance is designed to pay out a lump sum on the death or disability of the insured key person, during the length of the policy. It is paid as a lump sum and could significantly help the business to recover.

There are many ways to determine the need and quantify this in dollar terms. The method used will be determined by what makes the person important to the business. Your business risk specialist will assist you in this process.

For instance, the person has given a personal guarantee for a business loan or has given a director’s loan to the business, then the need is simply the amount outstanding under the loan.

In other cases, when determining the need, it may be necessary to take into account:

Basically, the factors which must be considered when determining the need are:

A company purchases an insurance policy on the key employee, pays the premiums and is the beneficiary of the policy. If that person unexpectedly dies or becomes disabled, the company receives the insurance.

From a taxation perspective, when structuring key person insurance it is particularly important to be clear about the purpose of the cover as this will affect the tax deductibility of the premiums, as well as the tax treatment of the insurance proceeds.

If the Trauma or TPD payment is to replace revenue it is considered assessable income. No CGT is applicable and the premium is deductible as an expense.

If the Trauma or TPD payment is to replace capital (ie. pay down a guaranteed debt) CGT would be applicable and the premium is not deductible as an expense.

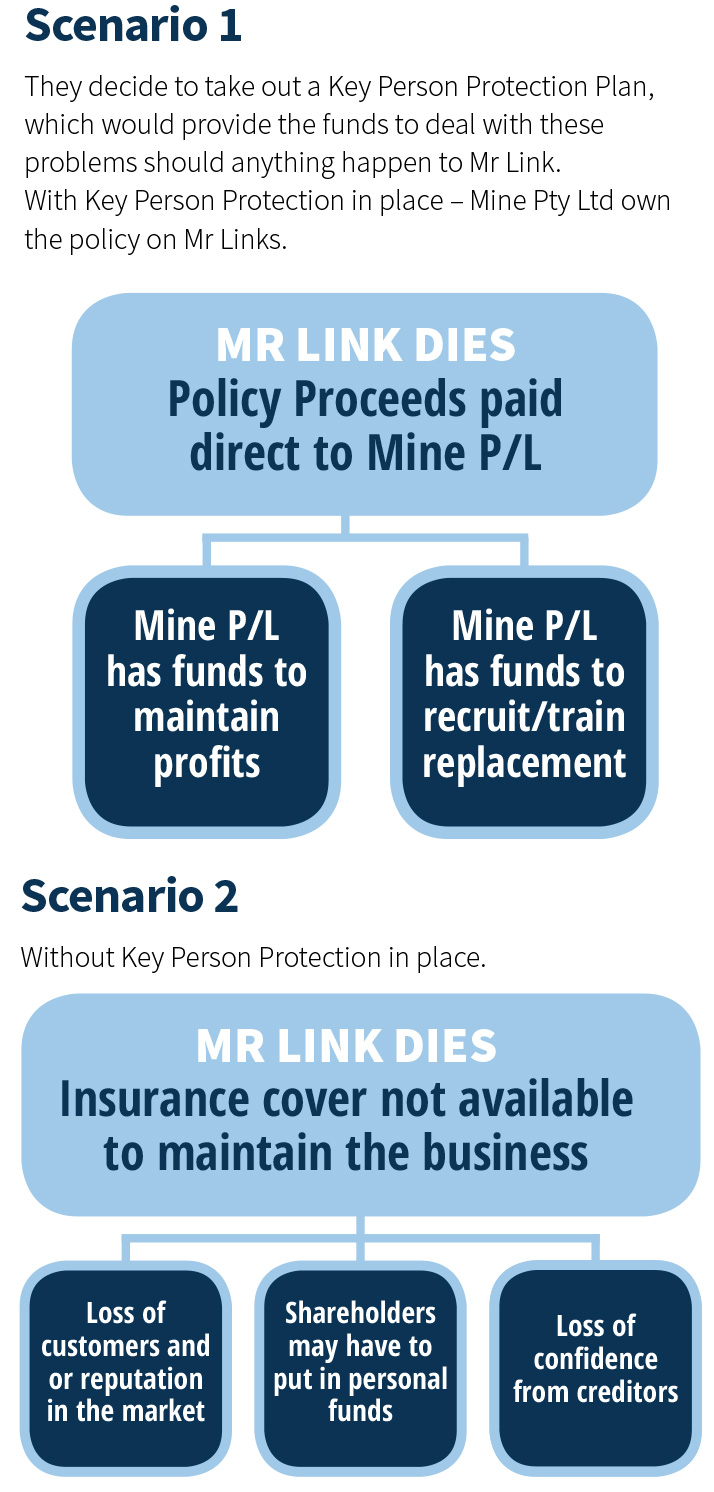

Mine Pty Ltd is a niche manufacturing business in specialist mining equipment. Mr. Link (industrial engineer) is employed by Mine Pty Ltd for his designing and developing expertise. The company’s sales rely on these customised machinery.

After recent discussions, the shareholders have realised that their business relies on Mr Link’s expertise and design capabilities. If he were to become critically ill or die during the next 3-5 years, their business could suffer and they could potentially lose up to 30% of their profits. In addition, they may have to recruit and retrain a replacement, which could take at least 1-2 years.