When two or more parties share the ownership of a business, they each own shares in a company or units in a unit trust that carries on the business.

In the event one party dies or becomes disabled the other parties want to ensure they are able to purchase the outgoing party’s interest and in turn the outgoing party wants to ensure that their estate is paid a fair value for their interest.

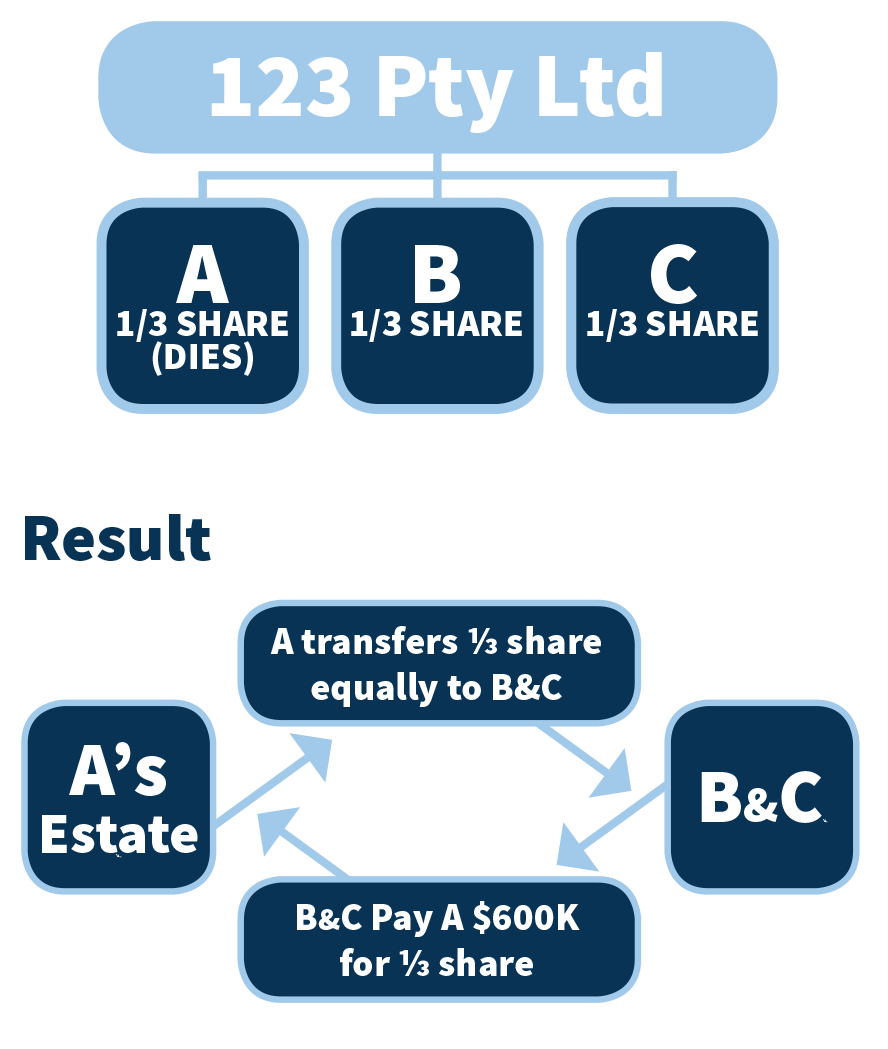

A, B and C own shares in 123 Pty Ltd, a management consulting business worth $1.8 million. They have a business succession (buy/ sell) arrangement covering death or disablement. “A” dies suddenly of a heart attack. Because an agreement is in place they should have a smooth transfer of ownership.

Business owners are utilising life insurance to provide the funds to purchase an outgoing owner’s interest. It is imperative that if the parties intend on using insurance to fund the transfer of shares, that there is a buy/sell agreement in place.

Assume Basil, Cybil and Polly own equal shares between them in ABC Pty Ltd. A Buy/Sell option agreement is in place that gives each of them the option of forcing the sale of their shares to the other should any one party die. Basil dies. Cybil and Polly exercise their option to purchase Basil’s share from Basil’s estate. (Alternatively, Basil’s executor could exercise the option to force Cybil and Polly to buy). The business is valued at $1.8m. Basil’s shares are worth $600,000. There is a life insurance policy in place on Basil for $600,000. The $600,000 is paid to Basil’s estate. Upon receipt of this money Basil’s executor must transfer Basil’s share to Cybil and Polly.

The purpose of a buy/sell arrangement is to ensure a fair outcome for the parties carrying on a business, in the event one of them die or become disabled. Examples of problems that can arise if agreements are not in place.